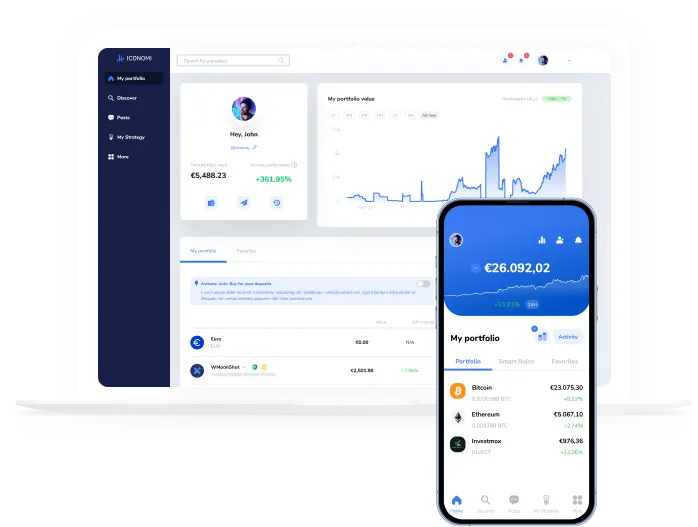

Easy way to invest in and manage your crypto

Rebalance your portfolio with one click

See platformInvest by copying a Crypto Strategy

See strategies

Instant deposits

€10,717,300

Who is it for

User-friendly Start to Crypto

Spend 80% less time on portfolio management every week

Put your crypto knowledge to your advantage

Diversify Investments or Use Co-Branded Solution

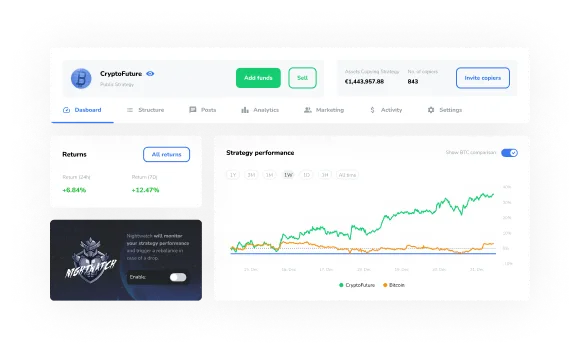

Start Investing by Copying Strategies

A Crypto Strategy is a collection of crypto assets chosen and led by a Strategist.

Crypto Strategies - like portfolios, but better

Crypto Strategies - like portfolios, but better

Buy Crypto

Buy Crypto

Easy to use platform features

Asset custody

Posts from Strategists

Read what our Strategists are saying about the market and the crypto sphere

Hello all,

I said 1 month ago, when this correction started that is no reason to panic. Buy if you have Cash or do nothing! No pannic sell! Enjoy your life! The real good things will come!

My strategy here: https://www.iconomi.com/asset/CRYPTOALLIEN

This modification ensures that the ratio can be calculated without encountering division by zero errors.

I made a slight adjustment to the ratio.

You know, some people might want to do this programmatically.

You know that the denominator and numerator cannot be zero, but we can also describe it mathematically by adding an infinitesimal value (like ϵ=10^ −6 or ϵ=10^ −9 or ϵ=10 ^−12) that does not affect the final result to ensure there is no zero.

Adding an infinitesimal value like ϵ ensures that we avoid division by zero errors while not impacting the final result of the calculation.

This approach maintains the integrity of the mathematical operations while accounting for cases where the denominator or numerator might approach zero.

So, by adding a very small positive value like ϵ , we ensure that the division is always well-defined and that our calculations proceed smoothly.

The numerator of the ratio measures the excess return of the asset over the risk-free rate, with a small value 𝜖 added to avoid zero denominators.

The denominator compares the excess return of the market over the risk-free rate, also with ϵ added.

The ratio of the standard deviation of the market to the standard deviation of the asset adjusts for the volatility of the asset compared to the market, with ϵ added to both standard deviations to avoid zero denominators.

If you apply the equation I shared you will be able to separate the assets very quickly which have value above 1:

◾A return equal to the market, but with less risk.

◾Higher return than the market, but with less risk.

◾A return higher than the market, but with risks similar to the market.

◾A return higher than the market with a risk higher than the market, but these returns are proportional to the risks.

Provided that the market return and the asset return are positive

https://www.iconomi.com/asset/MRJARADAT?postId=630d332a-b688-44ab-9eb5-0450a935b736

However, I am very open to discuss with everyone in mathematics and if you have a suggestion you can talk to me further.

And now 2 the sky

Up